LANGDON EQUITY PARTNERS - February 2023

Reviewing recent sea freight rates at surface level is not enough: The Devil is in the details

Reviewing recent sea freight rates at surface level is not enough. We analyze the complete picture and the impact on a sample of our companies.

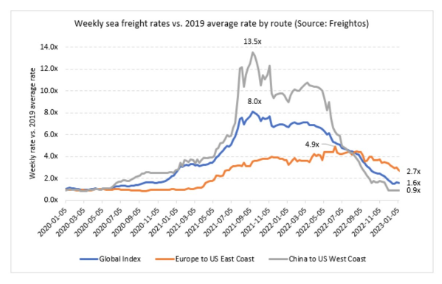

As a firm with a concentrated number of investments in our portfolios, we can spend time digging into the nitty-gritty details of our holdings. One of our most reinforced principles is to trust, but verify and sometimes, we find nuances in the details that challenge oversimplified headlines such as “Shipping rates are now back to pre-COVID levels” or “Supply chains upended by COVID are back to normal.” These broad statements typically refer to major routes out of a specific country or to congestion at specific ports, and are not indicative of the complete picture. While the price to ship a container out of China by sea has recently returned to pre-COVID levels (and even slightly below), westbound transatlantic (Europe to US East Coast) sea freight rates are nearly 3 times higher than the average rate in 2019, prolonging meaningful margin recovery for European exporters into the back half of 2023.

How does this impact our investments?

We focus on companies with low leverage and pricing power that are materially undervalued. Many of our investments in companies where freight is a big input cost have seen significant gross margin compression, which led to lower profitability in 2022. We believe that in the case of these investments(Thule, Fever-Tree, Royal Unibrew), this hit to profits will be transient as freight rates return to pre-pandemic levels. In the case of Royal Unibrew, they have also taken steps to localize production to their recently acquired, Canadian-based, Amsterdam Brewery facility. On the topic of localizing production, we recently saw one of our largest Canadian holdings, Waterloo Brewing, acquired by Carlsberg. It would seem reasonable to expect that more European manufacturers of relatively low value and bulky consumer goods are going to look for North American production capacity given the ongoing energy crisis in Europe and elevated sea freight costs.

As for sea freight rates themselves, the tide may finally be turning (pun intended)

In the absence of local production, the good news is that lower rates for routes out of Europe and margin recovery for European exporters is coming, and it may surprise people. Despite the higher demand on the westbound transatlantic lane, supply has remained roughly at 2019 levels throughout the pandemic. Asper Sea-Intelligence, operators will finally inject up to 30% more capacity (compared to 2019) to this lane by mid-February 2023. This supply increase already started in December, and rates are starting to turn. In our conversations with European exporters, they have shared with us that there is a false perception among investors that sea freight rates have already fallen, leaving them confused as to why margins have not yet recovered. This has created doubt that freight is the true cause for margin deterioration, and an opportunity for those that dig into the details.

Disclaimer:

This article is prepared by Langdon Equity Partners. Content in respect of the Langdon Smaller Companies Fund (ARSN 657 901 614 (the Fund) is issued by Pinnacle Fund Services Limited ABN 29 082 494 362 AFSL 238 371 (‘PFSL’) as responsible entity of the Fund. PFSL is not licensed to provide financial product advice. It contains general information only. It is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. It has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so.

Past performance is for illustrative purposes only and is not indicative of future performance.

While Langdon Equity Partners Limited (‘Langdon’) and PFSL believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Langdon and PFSL disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. This disclaimer extends to any entity that may distribute this communication.

For Australian Clients:

The Product Disclosure Statement (‘PDS’) and Target Market Determination (‘TMD’) of the Fund are available via the links below. Any potential investor should consider the PDS and TMD before deciding whether to acquire, or continue to hold units in, the Fund.

Link to the Product Disclosure Statement: here

Link to the Target Market Determination: here

For historic TMD’s please contact Pinnacle Client Service Phone 1300 010 311 or Email service@pinnacleinvestment.com

For Canadian Clients:

Important information about each Langdon mutual fund is contained in its prospectus, AIF, fund facts document and in its management report on fund performance. Any potential investor should review these documents prior to making any investment decision relating to such fund. You can view copies of these documents by following the links below:

Link to the Langdon Global Smaller Companies Portfolio Disclosure Documents: here

Link to the Langdon Canadian Smaller Companies Portfolio Disclosure Documents: here

Subscribe to our updates

Stay up to date with the latest news and insights from Pinnacle and our Affiliates.